Countries Most Exposed to the Flow Disruption in the Strait of Hormuz: The Geography of Fragile Energy Dependence

The Strait of Hormuz has long been treated as a geopolitical corridor, a narrow ribbon of water through which nearly a quarter of the world’s seaborne oil quietly passes. That framing no longer holds. In this cycle, it has become something more consequential and far less stable: a pressure point where supply constraints are no longer absorbed by inventories alone, but transmitted directly into how nations consume energy, how industries reorganize fuel use, and how households begin to quietly abandon oil altogether. What is unfolding is not just a disruption of flows, but a forced acceleration of transition, where demand destruction, electrification, and fuel switching are now moving in step with war risk, price spikes, and physical bottlenecks in global trade.

Strait of Hormuz | May 7, 2026 - The Strait of Hormuz is no longer merely a maritime chokepoint. In the current oil cycle, it has become the hinge upon which global energy stability swings—its narrowing lanes now amplifying price shocks, supply distortions, and structural demand rewiring across continents. As tanker traffic remains constrained and Middle Eastern exports are effectively throttled, exposure is no longer theoretical. It is uneven, sharply distributed, and increasingly consequential.

At the centre of this stress test sits a stark empirical reality: Asia carries the bulk of the burden, Europe follows at a distance, and the Americas remain comparatively insulated. But within that broad geography lies a far more nuanced map of vulnerability—one defined not just by volumes, but by dependency intensity, substitution capacity, and the physics of refinery compatibility.

The Strait as System Shock: Where the Bottleneck Begins

The Strait of Hormuz is, almost by design, a pressure valve between the Persian Gulf and global markets, at least since Iran became the Islamic Republic in 1979. In 1H25 (first half of 2025) alone, it carried about 20.9 million barrels per day of oil flows—roughly a quarter of global maritime oil trade and about 20% of global petroleum liquids consumption, according to the EIA. It is also the dominant corridor for LNG, handling over 20% of global LNG trade, with Qatar as the principal exporter.

But its strategic importance is not just in throughput. It is in concentration. According to the EIA, 89% of crude oil and condensate transiting the Strait goes to Asian markets, with China, India, Japan, and South Korea accounting for nearly three-quarters of those flows.

That concentration is what turns disruption into systemic shock.

As the International Energy Agency notes in its April 2026 Oil Market Report, the conflict-linked disruption has already triggered what it calls “the largest disruption in history,” with global oil supply plunging by 10.1 million barrels per day in March, while inventories outside the Middle East Gulf were drawn down by 205 million barrels in a single month. Brent crude, in this environment, has surged toward $130 per barrel, roughly $60 above pre-conflict levels.

This is not a price spike. It is a re-pricing of global oil logistics.

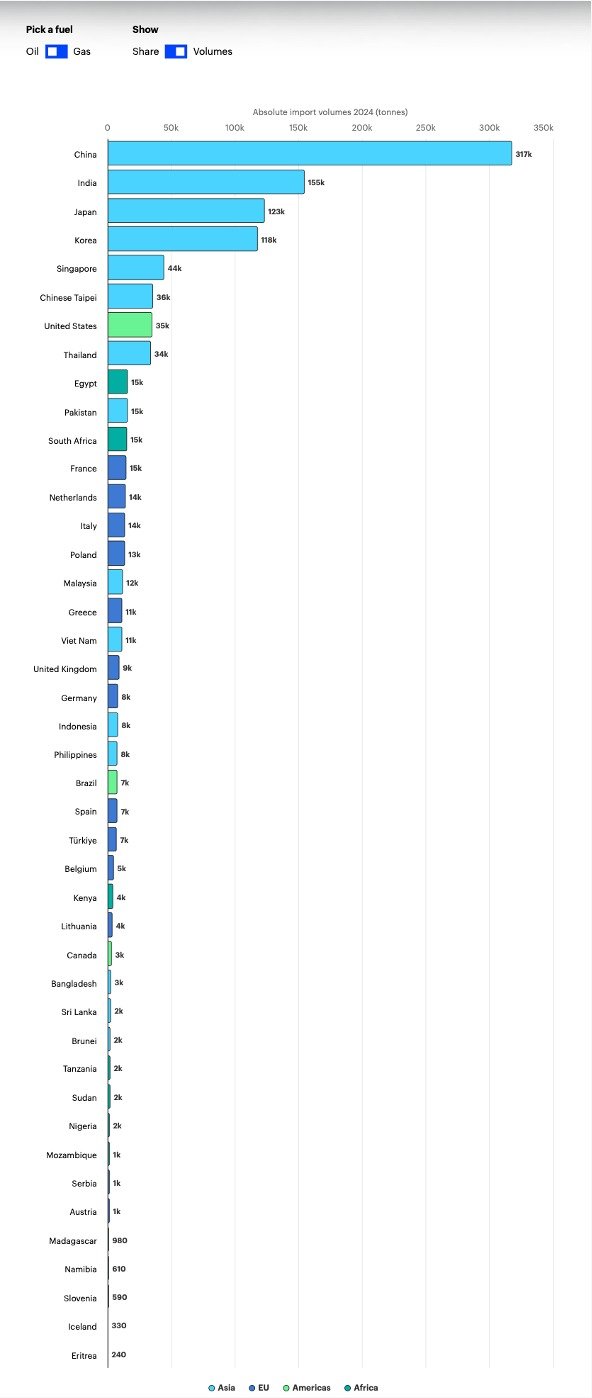

Oil Dependence: The Asian Gravity of Middle East Supply

If exposure were measured purely in tonnage, China would dominate the map. In 2024, it imported317,000 kt of oil from the Middle East, more than double India’s 155,000 kt and far ahead of Japan (123,000 kt) and South Korea (118,000 kt). These four economies alone anchor the physical demand base of Hormuz flows.

But volume only tells part of the story.

Dependency intensity reveals where stress becomes existential.

Japan sources 77% of its oil imports from the Middle East, South Korea 57%, Taiwan 63%, Pakistan 78%, Kenya 77%, and Thailand 50%. These are not marginal exposures. They are structural dependencies embedded in industrial energy systems with limited short-term substitution capacity.

By contrast, the United States sits at just 3% dependency, and most Western European economies range between 6% and 18%. Germany stands at 6%. The United Kingdom, 6%. France, 18%.

The divergence is not accidental. It reflects decades of Atlantic Basin diversification, shale expansion, and pipeline-integrated supply chains. As Michael Cembalest of J.P. Morgan notes, U.S. oil intensity has fallen “by half since then,”(referring to four decades prior, when he started working with JP Morgan), with the economy becoming significantly less oil-sensitive over the past four decades. Yet he also warns that “you can’t draw them down past a certain level” of global inventories, pointing to an emerging “operational stress point” by mid-2026.

In other words, resilience exists—but only within bounds.

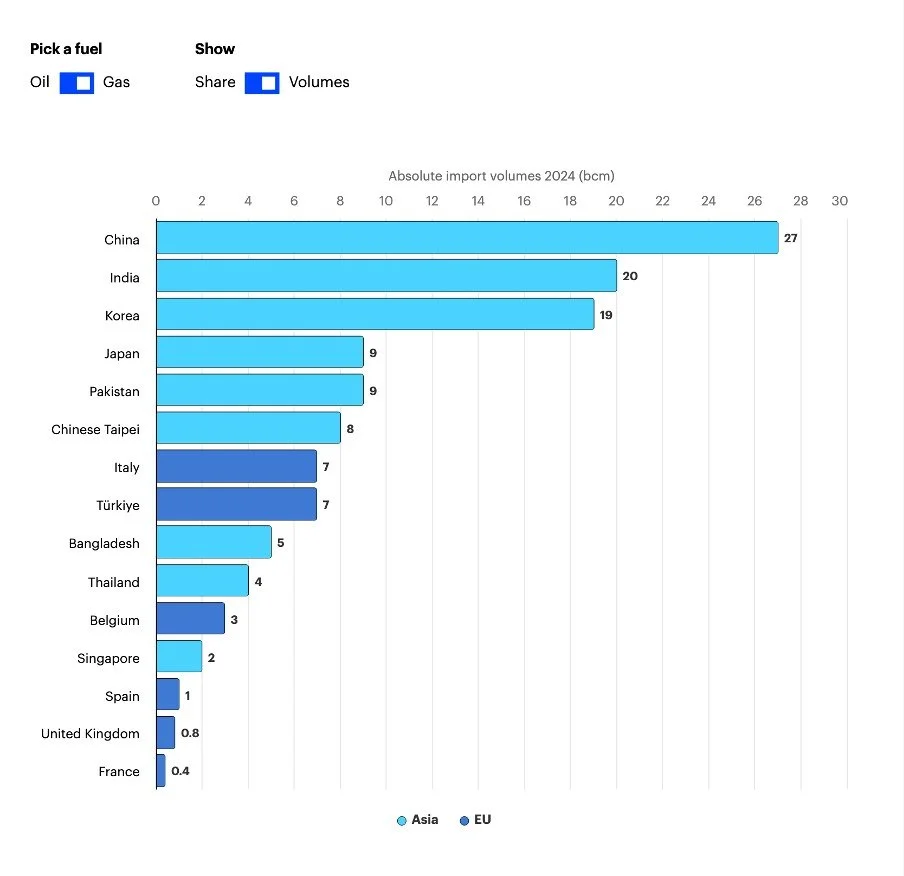

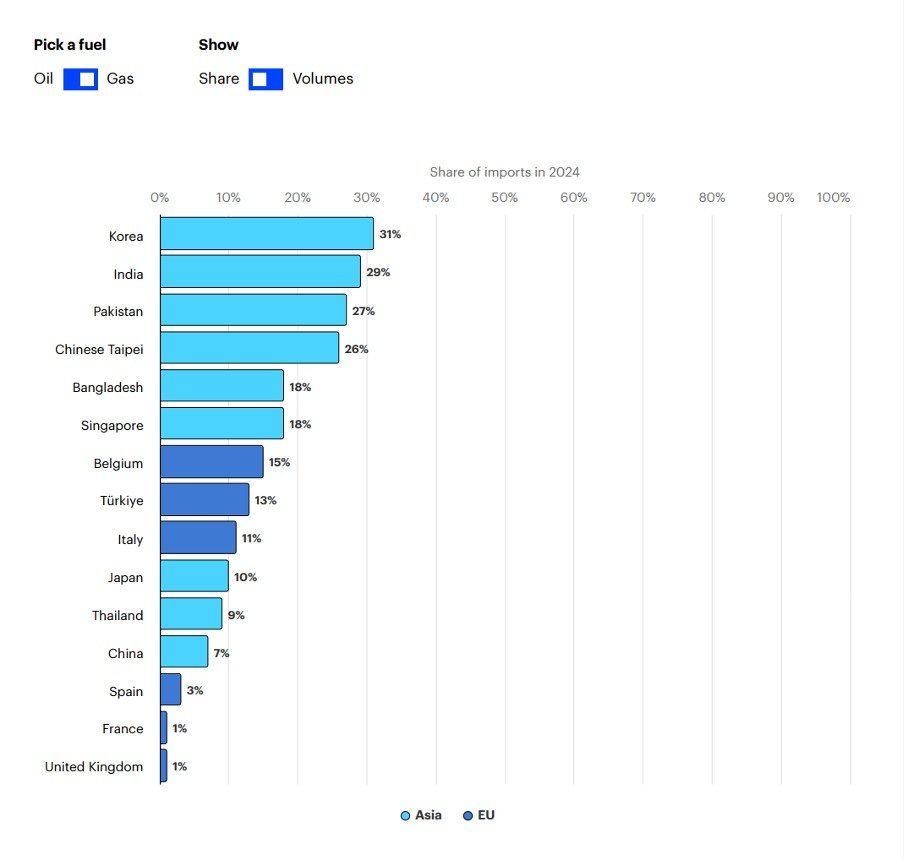

Gas Exposure: A Second Shock Layer Emerging

The gas market paints a more fragmented but equally consequential picture.

China leads with 27 bcm of Middle East gas imports, followed by India (20 bcm) and South Korea (19 bcm). But unlike oil, gas dependency is more fragmented, shaped by LNG competition from Australia, and the United States, with Qatar in the fray, of course, hampered by the current crisis.

Still, dependency ratios expose acute pressure points. South Korea again stands out at 31% gas dependence, India at 29%, Pakistan at 27%, and Taiwan at 26%. These economies sit in a narrow corridor where both oil and gas exposure overlap—creating dual-fuel vulnerability.

By contrast, the United States, Canada, and much of continental Europe are largely absent from Middle Eastern gas flows, reflecting the structural impact of domestic production and diversified LNG sourcing.

As Noah Brenner of Rystad Energy puts it, “without the Middle East, there are simply not enough molecules,” a constraint that is already “fueling high prices and demand destruction.”

Demand Destruction: When Prices Become Behaviour

What makes this shock different from earlier oil crises is that demand is not waiting for rationing. It is adjusting pre-emptively.

Lin Ye of Rystad Energy describes a Chinese market where “demand side conditions are deteriorating significantly,” despite price caps. Even with government intervention, “end user prices for gasoline, diesel, and jet fuel have still gone up and that’s led to visible demand destruction.”

That destruction is not abstract. It is behavioural. China alone has seen roughly 2 million barrels per day of oil demand disappear, driven by macro weakness, fuel substitution, and structural electrification.

That substitution is accelerating. Lin is explicit about the mechanism: higher fuel prices are pushing transport systems away from oil and toward electricity and gas alternatives. She captures the wave from her personal perspective: “I've always driven an EV, so I'm not contributing to oil demand apparently,” capturing a broader shift in consumption psychology that is now reinforced by macro deflationary pressure in China and rising energy costs across transport chains. In March 2026, 60% of heavy truck sales in China were LNG or new energy vehicles, up from 57% in February. That shift is not cyclical. It is cost-driven industrial migration.

As she notes, “the broader macro backdrop in China is still deflationary which is further suppressing consumption,” while policy intervention has only partially slowed pass-through effects. In other words, price is now destroying demand faster than policy can cushion it.

Market Stress: Refining, Storage, and the Physical Limits of Adjustment

The downstream system is absorbing the shock unevenly. Refining throughput globally has fallen by 1 million barrels per day in 2026, with Middle Eastern and Asian refineries cutting runs by about 6 million barrels per day due to feedstock constraints. Margins, however, have surged as middle distillate cracks reached record highs.

Yet the system is approaching physical constraints.

Cembalest warns that by June or July, inventories could hit “operational stress points,” beyond which “fuel rationing” becomes more likely, particularly in Asia and Europe. By September, he adds, the world risks falling below a critical inventory threshold where “demand destruction” becomes unavoidable.

This is the moment where financial markets meet physical scarcity.

The China Paradox and the American Exception

China sits at the centre of this paradox. It is the largest absolute importer of Middle East oil, yet its dependency ratio—38% for oil and 7% for gas—reflects diversification at scale. It is simultaneously exposed and buffered - simultaneously managing surplus, reallocating cargoes, and accelerating substitution.

According to Lin Ye, state refiners have begun reselling West African crude cargoes, tightening global differentials while adjusting domestic supply balances. At the same time, refined product exports are being recalibrated through quota adjustments.

The United States, meanwhile, represents the structural counterpoint. With just 3% oil dependency and negligible gas exposure, it stands insulated from direct supply shocks, even as inflation ripples through commodities. As Cembalest observes, higher oil prices are pushing up “fertilizers, methanol, jet fuel, shipping fuel… anywhere from 40% to 120%,” yet the economy remains resilient due to a long-term decline in oil intensity.

Still, resilience does not mean immunity. Inflation expectations are rising, and the Federal Reserve now faces a renewed inflation impulse precisely as energy markets tighten.

Africa’s Uncomfortable South-Eastern Exposure

Less visible, but highly exposed in dependency terms, are several African economies. Eritrea (91%), Madagascar (89%), Kenya (77%), Tanzania (53%), and South Africa (54%) rely heavily on Middle Eastern oil despite relatively small absolute volumes. These are systems with limited fiscal buffers, meaning price shocks translate more directly into transport costs, food inflation, and foreign exchange pressure.

The System Under Strain

Across the dataset, one pattern dominates: the Strait of Hormuz crisis is not uniform in impact. It is asymmetric, cascading through Asia’s industrial base, selectively tightening Europe’s gas-linked economies, and largely bypassing the Americas in direct supply terms.

Yet as Rystad Energy’s Priya Walia notes, the system is not only about volumes but “grade quality,” with Asian refiners reliant on specific medium sour crudes that cannot be easily substituted from Atlantic basins.

And as Brent Brenner summarises the broader equilibrium: “without the Middle East, there are simply not enough molecules.” That is the defining constraint - not scarcity alone, but mismatch. Not just shortage, but substitution failure. And in that gap between barrels available and barrels usable, the global oil system is currently being rewritten in real time.