America’s Hormuz-Free LNG Edge Takes Shape as TotalEnergies and Commonwealth Deepen the U.S. Export Stack

As Hormuz risk sharpens the premium on secure energy routes, U.S. LNG is emerging as more than a supply story. It is becoming a geopolitical advantage. TotalEnergies’ rise as the top exporter of U.S. LNG in 2025 and Commonwealth LNG’s move into full execution in Louisiana point to a larger shift: America is building a route-diversified LNG machine capable of serving Europe and Asia without passing through the Persian Gulf’s most vulnerable chokepoint.

Washington, USA | May 26, 2026 - The United States’ most potent LNG advantage is no longer just volume. It is geography. As the Strait of Hormuz reasserts itself as the world’s most exposed energy chokepoint, America’s Gulf Coast and Pacific-linked LNG buildout is becoming a strategic market-positioning win: a supply machine able to serve Europe and Asia without sailing through the Persian Gulf’s narrowest passage. The International Energy Agency says more than 110 bcm of LNG passed through Hormuz in 2025, representing almost one-fifth of global LNG trade, while around 93% of Qatar’s LNG exports and 96% of the UAE’s LNG exports transited the Strait. There are no alternative routes to bring those volumes to market.

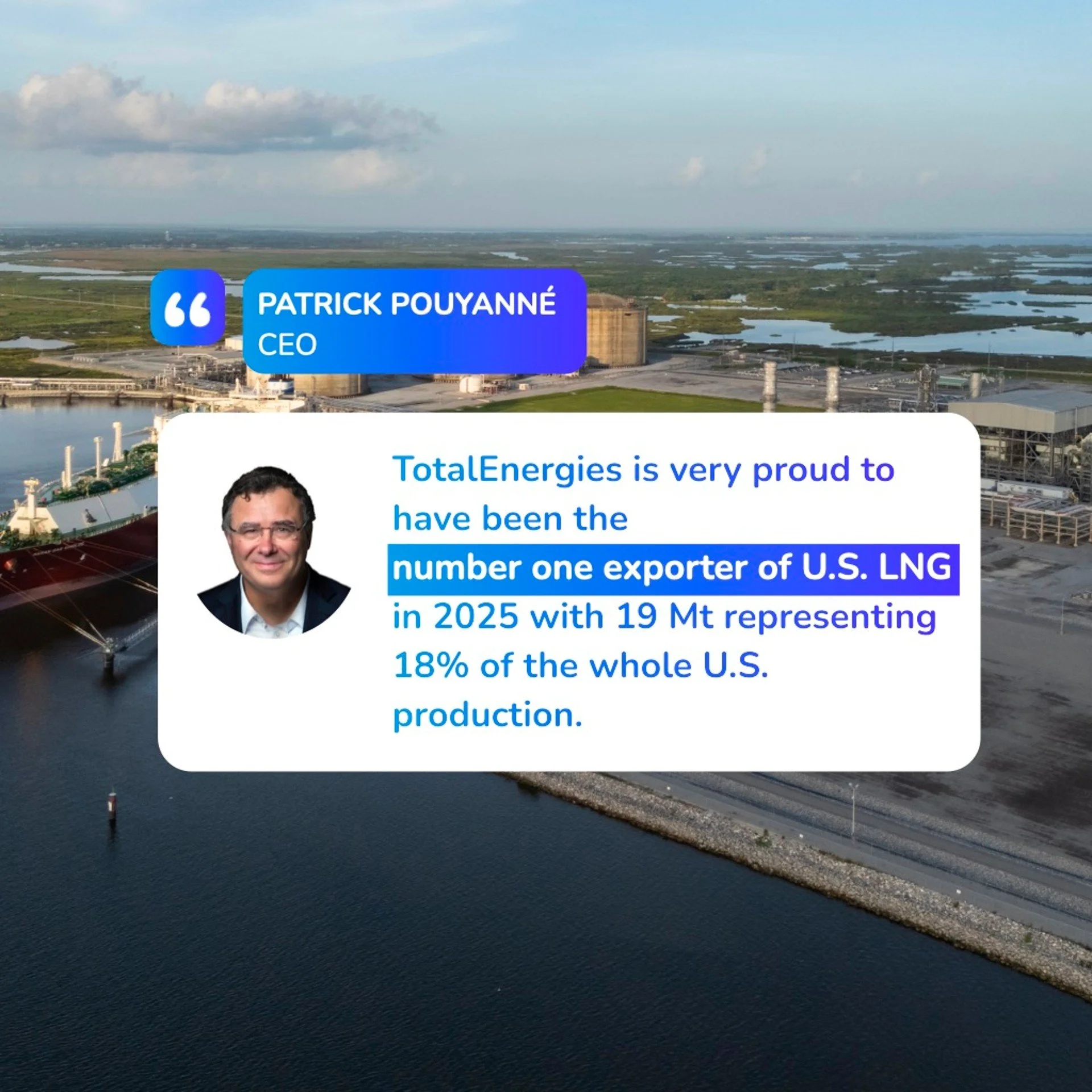

That is the opening through which U.S. LNG has moved from commercial growth story to geopolitical infrastructure play. TotalEnergies says it became the number one exporter of U.S. LNG in 2025, shipping 19 million tonnes, equal to 18% of total U.S. production. The company also says 14 million tonnes of those U.S. LNG exports went to Europe, underscoring how American supply has become a structural artery for allied markets after Europe’s long retreat from Russian pipeline dependence.

TotalEnergies’ U.S. LNG Lead Was Built Before the Crisis

TotalEnergies’ U.S. LNG position did not arrive suddenly. It was assembled through equity stakes, long-term offtake and a portfolio strategy that ties North American gas to European and Asian demand. The company says it is integrated across the LNG value chain in the United States, with upstream gas production assets in Texas and Oklahoma, offshore U.S. assets and investments in major North American LNG projects including Cameron LNG, Rio Grande LNG, Energia Costa Azul LNG and prospective offtake from Alaska LNG.

At Cameron LNG in Louisiana, TotalEnergies holds a 16.6% interest and exports more than 4 Mtpa from a facility that reached its 1,000th cargo milestone in July 2025, six years after its first commissioning cargo left the site on May 31, 2019. TotalEnergies’ wider U.S. LNG book also includes offtake from major terminals including Sabine Pass, Freeport and Corpus Christi, giving the company both equity-linked and contracted access across the American export base.

The next layer is Rio Grande LNG in South Texas. TotalEnergies and its partners reached final investment decision on Train 4 in September 2025, adding a roughly 6 Mtpa unit to Rio Grande’s first three trains, which are already under construction. TotalEnergies holds 16.7% of the first phase, expected to start operations in 2027, and will offtake 5.4 Mtpa from those first three trains. Train 4 adds another 1.5 Mtpa under a 20-year offtake agreement, pushing TotalEnergies’ expected U.S. LNG export capacity above 16 Mtpa by 2030.

The Pacific Option Changes the Map

The portfolio also stretches beyond the U.S. Gulf Coast. In Baja California, Mexico, Energia Costa Azul LNG (ECA LNG) gives the North American LNG system a Pacific-facing outlet. Sempra Infrastructure describes ECA LNG Phase 1 as a 3.25 Mtpa nameplate project designed to connect natural gas from the western United States to Asian, Pacific Basin and other international markets.

That Pacific orientation matters. TotalEnergies says its 16.6% stake in Energia Costa Azul gives it access to 1.7 Mtpa from the project and allows LNG to reach Asian markets without transiting the Panama Canal, reducing shipping costs and emissions. For a market increasingly forced to price route risk alongside supply risk, that is not a footnote. It is infrastructure geography becoming commercial leverage.

In February 2026, TotalEnergies moved further in that direction with a preliminary agreement with Glenfarne to offtake 2 Mtpa from the Alaska LNG project for 20 years, subject to final investment decision. TotalEnergies described Alaska LNG as the only federally authorised LNG export project on the U.S. Pacific coast, with planned capacity of 20 Mtpa and direct access to Asia, the world’s largest LNG market.

Commonwealth Moves from Decision to Execution

The latest signal that the U.S. LNG buildout is still deepening came from Louisiana. On May 15, 2026, Technip Energies said it had received full notice to proceed on a major engineering, procurement and construction contract from Commonwealth LNG, a Caturus company, for a 9.5 Mtpa LNG export facility in Cameron Parish. The notice followed Commonwealth LNG’s final investment decision, moving Technip Energies from initial activities into full project execution.

Technip Energies’ scope covers six identical liquefaction trains using its SnapLNG by T.EN modular and scalable solution. The company said the replicated single design is intended to accelerate project schedules, optimise costs and improve predictability at scale. It also said a “major” award represents more than €1 billion of revenue and that the Commonwealth award was recorded in the second quarter of 2026 in its Project Delivery segment.

Arnaud Pieton, Technip Energies’ chief executive, framed the project in energy-security terms, saying the Commonwealth LNG final investment decision was “a pivotal moment for this strategic project” and that the company expected to deliver “a highly efficient facility that will support reliable LNG supply and strengthen global energy security.”

Caturus cast the project as part of a broader wellhead-to-water strategy. The company says its platform combines Caturus Energy, formerly Kimmeridge Texas Gas, with Commonwealth LNG, a 9.5 Mtpa export terminal project on the U.S. Gulf Coast near Cameron, Louisiana. Reuters reported that Caturus approved construction after securing $9.75 billion in funding, with the total project cost expected to reach $12.5 billion including financing fees, and that the plant is targeted to begin operations by 2030.

The upstream side has also been reinforced. In April 2026, Caturus said it closed the acquisition of Galvan Ranch natural gas assets from SM Energy, taking net production above 1 Bcfe/d and placing the company among the top 10 private U.S. natural gas pure-play producers. That matters because the Commonwealth model is being sold not simply as another export terminal, but as part of an integrated natural gas and LNG platform with upstream supply tied to liquefaction capacity.

The Infrastructure Race Is Now Strategic

The Commonwealth milestone lands at a moment when LNG infrastructure is being recast as strategic insurance. The IEA says more than 110 bcm of LNG passed through Hormuz in 2025, with Qatar and the UAE heavily reliant on the route for LNG exports and no alternative route available for those volumes. That exposure is precisely why route diversity has become a premium feature in the LNG market, not merely a logistical detail.

The strategic implication is clear: U.S. LNG is not merely adding volume to the market; it is adding route diversity at a moment when Hormuz risk has become a pricing and security variable. Gulf Coast terminals such as Cameron, Rio Grande and Commonwealth do not replace Persian Gulf LNG molecule-for-molecule overnight, and U.S. projects still face execution, financing, permitting and downstream infrastructure constraints. But they offer something geopolitically priceless: supply that can be contracted by Europe and Asia without transiting Hormuz.

For Europe, that means another layer of insulation after the rupture of Russian pipeline dependence. For Asia, it means optionality in a market where Qatar remains a major LNG supplier and Hormuz remains a critical export corridor. For the United States, it is an export, diplomatic and industrial-policy win: gas produced in North America, liquefied through American-linked infrastructure and delivered into the world’s most contested energy markets with a route advantage Gulf producers cannot replicate.

TotalEnergies’ rise to the top of U.S. LNG exports shows how quickly that architecture is hardening. Commonwealth LNG’s final investment decision and Technip Energies’ full notice to proceed show the next wave is already moving from commercial ambition into engineering, procurement and construction. The lesson from Hormuz is not simply that the world needs more LNG. It is that the world needs LNG from more directions, through more routes, backed by infrastructure already in place before the next shock arrives.